How Credit Cards Were Invented: The Hidden History of a Predatory Debt System

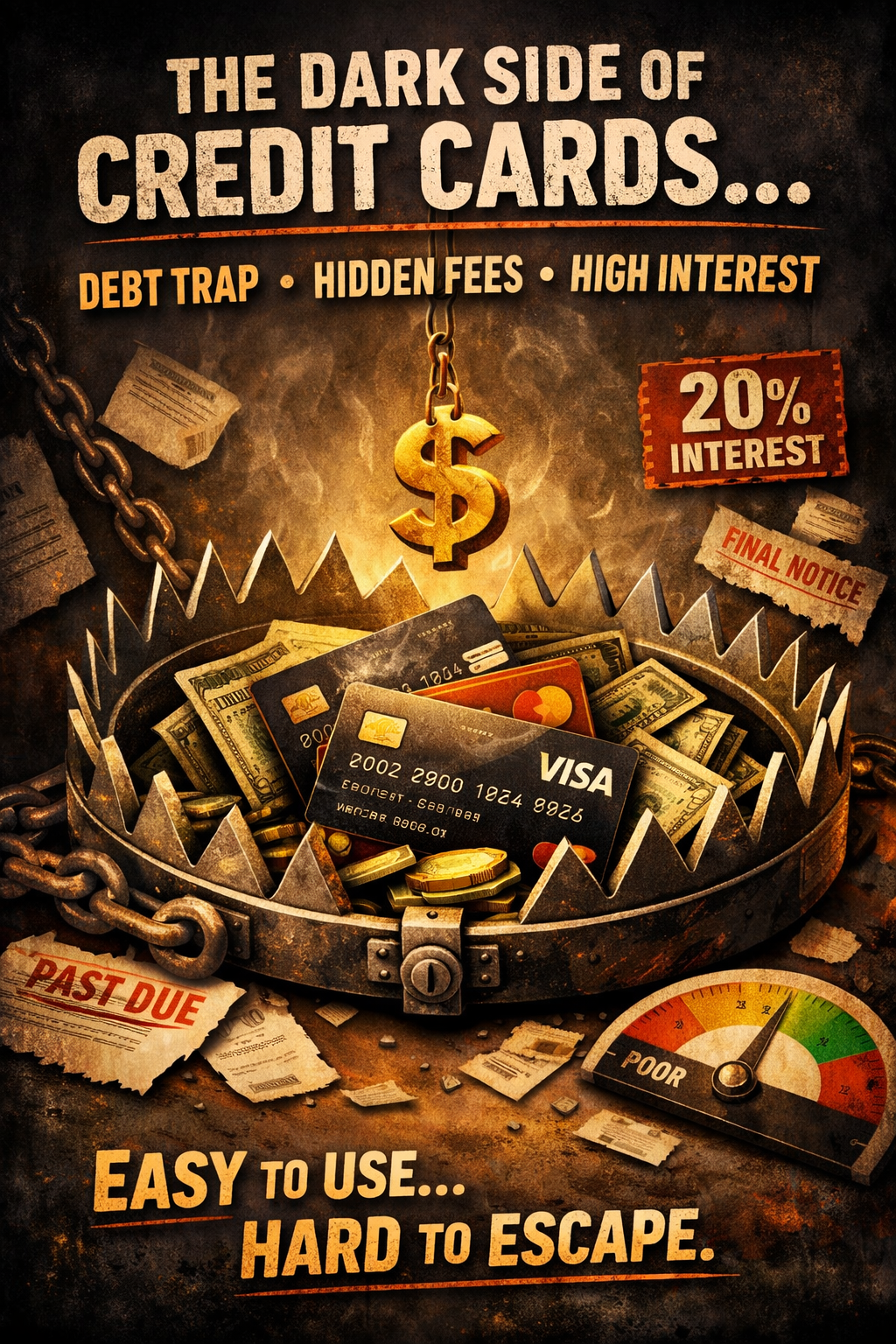

Credit cards are often marketed as tools of convenience and financial freedom. But the history of credit cards tells a very different story—one rooted in profit, control, and engineered debt.

The invention of credit cards didn’t happen to help consumers manage money better. It happened to extract value from spending behavior, normalize long-term debt, and turn everyday purchases into a recurring revenue stream for banks and credit card companies.

Understanding how credit cards were invented reveals why so many people today are trapped in revolving credit card debt.

The Early History of Credit Cards

Before modern credit cards existed, early forms of credit were limited to trusted customers at specific merchants. Department stores and hotels allowed wealthy patrons to buy now and pay later—no interest, no mass adoption, and no complex fees.

That changed in 1950 with the creation of Diners Club, widely considered the first modern charge card. While the origin story is often framed as convenience, the real innovation was inserting a third party between consumers and merchants—and charging both sides for the privilege.

This was the beginning of the modern credit card industry.

Revolving Credit: The Real Invention That Changed Everything

Early cards required full monthly payment, limiting profits. The breakthrough came when banks introduced revolving credit, allowing cardholders to carry balances and pay interest.

This single change transformed credit cards from payment tools into long-term debt products.

Banks quickly realized that:

- Customers who carry balances generate the most profit

- Interest compounds faster than most consumers realize

- Minimum payments keep debt active for years

By the late 1950s, Bank of America launched BankAmericard, which eventually became Visa. Soon after, Mastercard entered the market.

Credit cards were no longer optional—they were aggressively distributed.

How Credit Card Companies Normalized Debt

One of the most predatory aspects of credit card history is how debt was rebranded as responsible financial behavior.

Credit card companies introduced:

- Low minimum payments that stretch debt across decades

- Teaser interest rates that spike after habits form

- Rewards programs that encourage overspending

- Late fees and penalty APRs that punish mistakes

These features weren’t designed to help consumers avoid debt. They were designed to keep balances active.

In the credit card business model, paying in full is the exception—not the goal.

The Psychology Behind Credit Card Spending

Credit cards fundamentally changed how people spend money. Swiping a card removes the immediate emotional impact of paying, making purchases feel painless.

This psychological separation:

- Encourages higher spending

- Reduces price sensitivity

- Makes interest charges feel abstract

- Weakens cash discipline

Over time, this led to rising household credit card debt and increased dependency on borrowing for everyday expenses.

Why Credit Cards Are Considered Predatory by Critics

Critics argue that credit cards qualify as predatory lending tools because:

- Interest rates regularly exceed 20%

- Fees are complex and difficult to track

- Credit scores are used as leverage, not protection

- Financial literacy gaps are exploited

Consumers often agree to terms they don’t fully understand, while credit card companies rely on that confusion for profit.

The system doesn’t collapse when people struggle—it thrives.

The Legacy of Credit Cards in Modern Finance

Today, credit cards are embedded in nearly every part of the economy. Prices are inflated to absorb merchant fees. Debt is normalized. Financial stress is widespread.

Yet the core design hasn’t changed since the beginning:

- Encourage spending

- Delay consequences

- Profit from carried balances

Credit cards weren’t invented to empower consumers—they were engineered to monetize debt over time.

Final Thoughts: Understanding the Real History of Credit Cards

The true history of credit cards isn’t about convenience—it’s about control, profit, and psychological manipulation. What started as a niche payment method evolved into one of the most powerful debt systems in modern finance.

Once debt became normal, it became permanent.

And that may have been the plan all along.